Time to Displacement

A Model for Measuring When AI Threatens Your Business.

04 - The Canary Papers: Time to Displacement (Download PDF)

In January 2026, at the World Economic Forum in Davos, Ken Griffin dismissed artificial intelligence as impressive on the surface and hollow underneath the moment you looked closely. He had been one of the most prominent skeptics in finance, and the dismissal was in character. Four months later, at Stanford, he reversed himself entirely. Work that Citadel would once have handed to teams of master's and PhD finance professionals, work that took weeks or months, was now being done by AI agents in hours or days. These were not mid-tier roles, he said, but some of the most highly skilled jobs in the firm. He described going home one Friday fairly depressed.

The interval between those two positions was four months.

I have not been able to stop thinking about that interval. Not the reversal itself, which is becoming common enough that it barely registers, but the speed of it: a serious, skeptical, extraordinarily well-informed operator going from dismissal to alarm in a single quarter. That is the part the human mind handles badly. We can understand acceleration as a concept and still be blindsided by it in practice, because we reason in straight lines and an exponential curve does not.

This paper has had a long gestation, longer than the three before it. The others came relatively quickly once the argument was clear. This one resisted, because the question underneath it resisted. The next decade will not deliver the progress of a century. It will deliver the century. The wealth created and the businesses built, and on the other side of the ledger the collapses, the dismantled livelihoods, the sectors that vanish before they understand they are being displaced. A century of both, compressed into ten years.

That compression does not arrive evenly, and the unevenness is the whole point. Some businesses will feel it as a slow tightening, manageable with adjustments at the margin. Others will wake up inside a market they no longer recognize, facing competitors they have never heard of and economics that no longer work. The difference between the two is not random. It is structural, observable, and, I would argue, measurable.

The first three papers in this series circled the pace from different angles. Paper 01 treated the compression as a thought experiment. Paper 02 measured the distance between what AI can already do and what organizations are actually doing with it. Paper 03 turned the lens outward, to the labour markets, consumer capacity, and trust infrastructure that every business quietly depends on. What none of them answered is the question executives actually ask me, once the polite interest and the AI strategy talk and the question of which LLM to give their teams are out of the way, usually about forty minutes in.

How long until AI threatens my business?

Not how will AI change the industry. Not what should the AI strategy be. How long. Before it matters. Before it is real. Before the competitor I have not heard of yet shows up with a product that does what my team does, faster and cheaper, and funded by people who understand something I do not.

That question is the one the Time to Displacement model, or TTD, is built to answer. Time to Displacement is not a prediction that the company will fail, lose all its customers, or go out of business on a specific date. It is an estimate of when the competitive conversation changes. Before the displacement point, customers are choosing between the company and the traditional way of doing things. After the displacement point, customers are choosing between the company and AI-powered alternatives that did not previously exist.

The unevenness of that shift shows up immediately. The SaaSpocalypse of February 2026 did not arrive on schedule, and a lot of analysts concluded it was overcalled. The signals have been there for a long time. Satya Nadella said in late 2024 that the SaaS layer of the organization would be replaced by the AI layer, and the comment caused a ripple but not a wave. Scott Brinker's MarTech map ballooned past fifteen thousand solutions, you need a magnifying glass to read it, and the assumption was that the map would keep expanding indefinitely. It will not. The map had its expansion phase. The contraction phase has barely started, and when it does start, it will not be uniform across the board. Some categories will collapse. Others will hold. The companies that are paying attention know which they are. The companies that are not, do not.

The catalogue of frameworks

Anyone serious about AI strategy has been through the existing catalogue of disruption frameworks. Schumpeter's creative destruction remains useful as philosophy, but it was written before the internet existed and offers nothing operational to a CEO planning five years out, never mind eighteen months. Cisco's Digital Vortex maps industries on a grid of disruption magnitude and time horizon, intuitive but coarse. BCG's Consumer AI Disruption Index ranks sectors by AI vulnerability. Reforge's AI Risk Assessment is more granular and practical but stops short of converting exposure into a timeline.

These frameworks share a common limitation. They measure industry-level exposure but not company-level vulnerability. They tell you the storm is coming. They do not tell you whether your roof holds. Most treat AI adoption as binary when it is actually a spectrum with compounding non-linear effects. None incorporate volatility, the possibility that a capability release or a funded entrant could compress any timeline overnight. And none separate passive defense, the moats and switching costs a company has, from active defense, the AI transformation it has actually undertaken.

The AI labs themselves have failed to convey the urgency in a way that lands in a boardroom. They publish benchmark improvements. They publish capability curves. Neither translates into what it means for a CEO's Tuesday. The researchers know the pace. The venture capitalists funding AI-native competitors know it, that is why the funding is moving the way it is moving. The executives across the table do not. They have read the same articles, attended the same conferences, and come away with the same composite of important, intensifying, hard to operationalize. A chart showing that GPT-5.5 outperforms GPT-5.0 on a reasoning test does not tell a CEO in manufacturing or insurance or retail what it means for the business they are responsible for protecting.

The gap between knowing AI is important and knowing how much time you have is the gap TTD is built to close. It does not close it perfectly. No single number could. What it does is convert a vague unease into a structured estimate, sector by sector, company by company, of when AI alternatives become real enough to change the competitive conversation. The number is a starting point for a strategic conversation that, in most boardrooms today, is not happening with enough rigor.

The moves that produced the model

The decision I made when I started building was to construct a model rather than another framework. A framework names risk. A model returns a number. Returning a number is harder, because the number can be wrong and the math has to defend itself, but the discipline of returning a number forces every strategic question into the open. “We are exposed to AI” is a sentiment. “We have 2.3 years before our consumer business is structurally displaced” is a decision-forcing claim. The boardroom does different things with the two.

The architecture is a four-term composition: Industry Baseline × Structural Defense × AI Maturity Multiplier × Volatility Compression. Each term addresses a distinct reason the displacement gap closes faster for some companies than others. The full mathematical apparatus lives in the methodology companion. What follows is the moves that produced the four terms, because those moves are where the model differs from anything else in the strategic catalogue.

The first move was to adapt the volatility concept from options pricing. Black-Scholes lives or dies on its volatility input, conventionally written as sigma. In financial markets, volatility is symmetric, prices move up and down around a drift. AI capability volatility is not like that. It is asymmetric. Capabilities jump upward and never regress. When a foundation model release improves coding performance by twenty points on a benchmark, the new capability is the new floor. The next release improves it further. The model captures this asymmetry by treating the volatility term as a compression-only multiplier. It can shorten a timeline but never extend one. Borrowing the concept from Black-Scholes was straightforward. Recognizing the asymmetry and engineering around it was the move.

The second move was to separate passive defense from active defense and treat them as independent layers. Moats, brand, switching costs, regulatory protection, contractual lock-in, are passive. They slow the attacker. AI Maturity, or AM, is different. A company that genuinely rebuilds itself around AI is not just defended; it has become a different competitive entity. Every framework I read collapsed these into a single AI readiness score, and the result was that companies with thin moats and deep transformation looked identical to companies with strong moats and shallow transformation. They are not. The model treats them as independent multipliers because they are doing different work.

The third move came from a diagnostic mistake I kept making. Early on, I was scoring companies by their most visible activity. Disney looked like a media company. A creative agency with an architecture practice looked like a creative agency. A recruitment firm with licensed immigration consulting and physical integration services looked like a staffing firm. The scores were systematically wrong in the same direction: over-counting digital exposure, under-counting physical and regulatory protection. The fix was a structured pre-scoring step I call the Value Chain Audit. Before any structural scores are assigned, every distinct activity is inventoried and weighted by revenue. The audit forces the analyst to account for the full range of the business rather than pattern-matching to an archetype. Disney's TTD moved from 3.4 years to 11.7 once the audit was applied, same company, same model, an entirely different strategic story.

The fourth move was to extend the volatility layer forward. Current domain volatility, observable benchmark improvements, displacement events in the sector, augmentation-to-automation migration, is one component. The second is the horizon factor, and it is the component the existing literature handles worst. Humanoid robotics is near a production threshold; Figure and Unitree are making leaps that change the supply curve for embodied AI labour. Agent-to-agent commerce is closer than most strategic conversations acknowledge; the moment AI purchasing agents become competent, brand loyalty, customer inertia, and pricing opacity all erode at the same time. These are not speculative. They are being priced into the model now, because a timeline that ignores them assumes the world stops where the foundation models currently are. It will not.

And then there is the Tuesday risk. Anthropic's release cadence is producing strategic events on a weekly schedule. Recent releases targeting creative, finance, and small business workflows have changed the competitive position of entire categories. Figma's stock dropped on the creative release. Jasper was a well-funded venture-backed company built around generative AI for marketing copy; with Claude Co-Work in market, Jasper’s strategic question shifts from growth to defensibility: what proprietary workflow, data, distribution, or trust layer does it own that Claude does not? The volatility layer captures this through elevated horizon sigma, but the underlying mechanism is worth stating plainly: in fast-moving industries, a Tuesday product release can render parts of a business structurally obsolete. AI Maturity transformation cannot address that risk. Only structural repositioning can.

The four layers, briefly

Industry Baseline is the weather. How fast is AI closing the gap in the sector? The Anthropic Economic Index enters the model directly here: theoretical coverage of work tasks against observed coverage. In computer and math occupations, the theoretical ceiling is around ninety-four percent and observed penetration is around thirty-three percent. In construction, both numbers are below twenty-five. Software and SaaS scores 8.0 on the model's velocity scale. Education Services sits at 7.4. Construction scores 2.1. This is the variable a company cannot change. The industry baseline is what every company in the sector is breathing.

Structural Defense is captured in a Structural Risk Ratio, the ratio of forces accelerating displacement (value chain digitization, revenue concentration risk) to forces slowing it (moat strength, customer relationship depth). When the ratio exceeds 1.0, structural exposure dominates structural defense. This is also where the Value Chain Audit does its work, without the audit, this layer produces the most systematic scoring errors.

AI Maturity is the lever the company controls. It enters as an independent multiplier, separate from structural defense, because it does different work. The non-linearity of the multiplier matters: the jump from AM 3 to AM 5 barely moves the number. The jump from AM 7 to AM 9 reshapes it. Surface-level AI adoption, chatbots in customer service, copilots for individual employees, provides almost no protection. Deep transformation, AI embedded in the product, the operating model rebuilt around it, provides years of additional runway.

Volatility compresses the timeline. Three components, macro acceleration, current domain disruption, and the forward-looking horizon, blend into an effective sigma that pulls Time to Displacement toward shorter intervals. The macro component is anchored quarterly. In Q2 2026 it sits at 6 on a 10-point scale: rapid advancement, frontier models broadly deployed, but no discontinuous capability jump in the past six months large enough to justify a crisis-level reading. The domain components vary by sector and by company.

These four layers multiply. The result is a number, in years, with associated risk tiers, Critical under two years, High two to five, Moderate five to ten, Low above ten. The methodology companion has the math. What follows is what the model actually says about a specific company.

One caveat matters more than the others. The model is decoding a rate of change that is not merely fast but exponential, and that is hard to feel and harder to appreciate. Think back to May 2025 and ask whether you would have believed Anthropic's first five months of 2026. Remember how quickly Griffin went from dismissal at Davos to alarm a quarter later. Treat any Time to Displacement number as a structured estimate: useful at the moment it is taken, most powerful in comparison with other scenarios, and already moving as the underlying capability curve changes.

The combined Coursera

On May 11, 2026, Coursera completed its $2.5 billion all-stock combination with Udemy, bringing together 290 million learners, 18,000 enterprise customers, 95,000 instructors/content creators, and hundreds of university and industry partners. Coursera CEO Greg Hart told Axios that AI is moving faster than reskilling programs. The CEO of one of the largest online learning companies in the world is explaining a defensive merger by pointing to AI capability outpacing his own product. He is, in effect, using the model's logic without using the model. The interesting analytical question is what the model says when it is actually run.

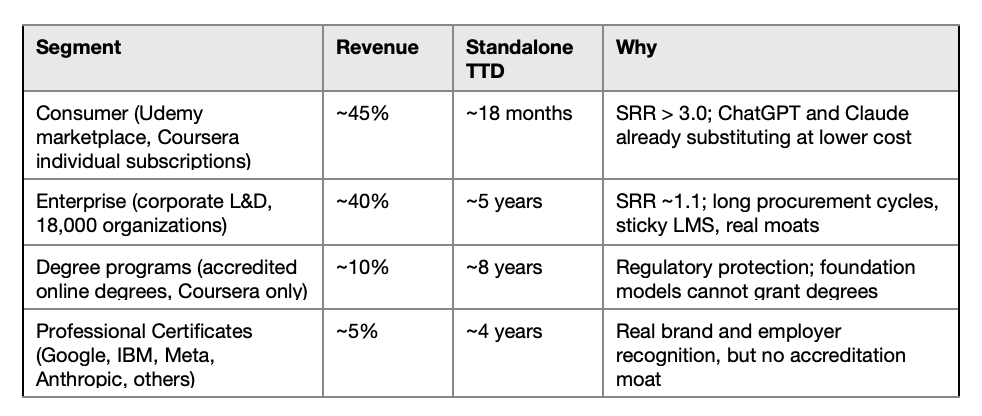

Surface scoring puts the combined company in trouble. Education Services sits at the boundary of Critical and High in the dataset, and a naive blend of Coursera's 2.3-year standalone and Udemy's worse score lands somewhere around 1.5 years, Critical, no recoverable position. The Value Chain Audit produces a different picture. The combined company is four businesses, not one.

Exhibit 1: Revenue-weighted TTD estimate for the combined Coursera/Udemy entity

Revenue weights are directional estimates for model illustration and should be updated as post-merger segment reporting becomes available.

Blending the four segments by revenue weight produces a combined industry baseline of 3.7 years and a Structural Risk Ratio of approximately 1.9. The merger does not change the composition, it doubles down on it. Udemy's consumer-heavy business raises the weighted exposure; Coursera's enterprise and degree businesses pull it back. The combined company is slightly more consumer-weighted, and therefore slightly more exposed, than Coursera alone.

AI Maturity is where the analysis surfaces something uncomfortable. Coursera has shipped an AI tutor, AI personas for soft-skill practice, an AI course builder that has cut course creation time by 87 percent, and AI translations across 4,500 courses. It is one of seven launch partners in OpenAI's apps platform; Anthropic is a content partner. By any reasonable measure, Coursera is one of the most AI-mature companies in Education Services, AM 6.5 in the model's scoring. And the lever is dampened. Pushing to AM 8 might add a year and a half. AM 9 might add two and a half. Real, but not enough to fix the underlying problem. The product itself, structured digital learning content, is the thing being commoditized. Coursera is already a fast adopter. That is part of why it survives. It is not why it thrives.

The volatility layer is doing the most work in this analysis. Effective sigma lands at approximately 6.8, driven by stock crashes and consumer revenue decline in the current domain, and by continuous foundation model improvement, agentic learning systems that turn the content provider into a commodity backend, and the institutional trust argument from Paper 03 in the horizon.

The Time to Displacement composition arrives at 2.2 years. High tier, close to the Critical boundary, slightly worse than Coursera was on its own. The merger does not fix the structural problem. The bigger lever is structural repositioning, shifting revenue weight toward degree programs and enterprise contracts, and away from the commoditizable consumer business. This presupposes the continued value of a degree in an AI world. Hart's public emphasis on rigorous credentials and the OpenAI and Anthropic partnerships are attempts to become the credential and verification layer for AI-mediated learning, rather than the destination platform. The model cannot tell you whether the bet works. It can tell you why it is the right bet to make.

The Disney contrast

On the surface, Disney is a media company. By instinct, an analyst would put it in that bucket and arrive at a Critical or High tier timeline. The initial scoring, before the Value Chain Audit, produced exactly that: a Time to Displacement of 3.4 years.

The Value Chain Audit forced a different question. What is Disney actually doing for revenue? The audit broke the company into its real operating segments and weighted them by contribution: roughly 40 percent from parks and experiences, 30 percent from media networks and streaming, 20 percent from studio entertainment, and 10 percent from consumer products and direct-to-consumer commerce. The parks division alone has a baseline closer to 8 years. Physical theme parks are not substitutable by AI. The streaming and studio operations sit closer to the media baseline, with TTDs in the two-to-four-year range. Re-weighting these to match the actual revenue mix produced a blended TTD of 11.7 years. Same company, same model, a different number, because the company was finally being measured as what it actually is rather than what it looks like from a marketing distance.

The strategic question for Disney is opposite of the one for Coursera. Disney's structural position is sound. The risk is complacency. The company's current AM score is roughly 4.5, meaningful but not transformative. The sensitivity analysis shows what AM transformation would buy: at AM 7, Disney's TTD extends to roughly 16 years. At AM 9, it approaches 22. For a company in a long-baseline industry with strong physical moats, the AM lever has enormous marginal return. Disney is not at risk in 2026. The question is whether the structural advantage gets compounded by transformation or coasted upon.

Which lever to pull

The two examples surface the model’s central strategic claim: the question is not whether to invest in AI. The question is which lever the investment should pull. The model clarifies which lever matters most.

For companies in slow-moving industries with strong structural defenses, Disney, Boeing, Deere, the AM lever has massive marginal return. Every point of AI Maturity buys years of additional runway, because the industry baseline is long and the structural position is defensive. Transformation here is not survival. It is a way to compound structural advantage into generational value creation.

For companies in fast-moving industries where the underlying product is being commoditized, Coursera, Salesforce, the entire SaaS cohort, the AM lever is dampened. These companies are often already AI-mature; further transformation adds incremental years but does not solve the underlying problem. The strategic move is repositioning: changing what the company sells, who it sells to, or where it sits in the value chain.

There are also cases where neither lever works. For some companies, Chegg, BuzzFeed, Gannett, pushing AI Maturity to its ceiling adds less than a year, and there is no defensible position to reposition into. The Structural Risk Ratio is so extreme, the industry velocity so high, and the competitive alternatives so direct that the displacement gap has essentially closed. The honest conversation is about pivoting or selling while there is still something to sell.

The model treats one further category carefully: the AI-native company. NationGraph at AM 8.8 sits at 1.6 years. Runway at a perfect AM of 10 sits at 2.5. Harvey AI at AM 9.1 sits at 4.0. These are companies using AI as well as it can be used, and they are being displaced anyway. They lack the scale, switching costs, and contractual lock-in that established competitors possess. AI-native is not a synonym for AI-safe.

What to do with the number

There is an irony in all of this that the model surfaces unavoidably. The biggest barrier to being displaced by AI is to adopt AI deeply enough to change the company itself. Not a moat. An extension. A company that genuinely transforms itself around AI buys runway it would not otherwise have, and the runway is real. But in the extreme tail of AI innovation, the world of transformative machine intelligence that sits 25 or 50 years out, business as we currently recognize it may not exist, and that is not the strategic question for the next five years. The strategic question for the next five years is what the company does with the runway it can still extend.

TTD is not a death sentence. It is a measure of strategic urgency. It is interpreting the exponential. The distinction matters because a number that feels like a sentence produces paralysis, and paralysis is the worst possible response to a closing displacement gap. The model is designed with a self-fulfilling dynamic in mind. A company that sees a short TTD and invests aggressively in the right lever extends its timeline. The intended effect is to motivate the action that renders its own prediction less accurate. Change the structural position. The number changes. That is the point.

The sensitivity analysis is the strategic centerpiece of every TTD calculation. It is what turns the model from a diagnostic into a decision framework. Showing an executive the difference between their company at different AM scores, or at different revenue mixes, or with different structural positions, in years of runway, is the moment the conversation usually shifts. Until that point, AI strategy is an abstract good. After it, AI strategy has a price tag and a payoff in concrete years.

The closing question

Return to where this paper began. A century of progress in a decade. The compression is uneven. Some businesses feel it as a slow tightening. Others find themselves in a market they no longer recognize. The difference between the two is not random. It is structural, observable, and, with the right instrument, measurable.

The first three papers in this series argued that pace matters, that the gap between capability and adoption is the defining feature of this moment, and that the systems beneath every business are restructuring around AI. Paper 04 offers the instrument. Not a prediction. A model for converting the displacement gap into a company-specific timeline, and the timeline into a set of strategic levers.

The organizations that captured the full value of electricity were not the first to install lights. They were the first to consider the electric motor and reorganizing production. The Time to Displacement model is a way to measure how much time you have to rethink yours, and what that rethinking is worth, in years.

The honest answer to how long do I have is no longer a finger in the air, wondering which way the wind is blowing. It is a number, a set of levers, and a choice.

A Counterargument

The Single Clock

A Response to “Time to Displacement”

The strongest challenge to Paper 04 is not that AI displacement is exaggerated. It is that the model is more persuasive than it is reliable, and the reason is not a flaw in the arithmetic. It is the decision to express a many-forced process as a single number on a single axis. The false precision the model risks is not incidental to that decision. It is produced by it.

Displacement runs on more than one clock, and the model reports only one.

The paper defines the displacement point cleanly: the moment customers stop choosing between the company and the old way and start choosing between the company and what AI has made possible. But that moment is governed by at least three timelines that do not move together. AI may be technically capable of the work in twelve months, economically compelling in twenty-four, and socially acceptable, to customers, regulators, employees, and the courts, in seven years. The capability clock is the one the model reads most confidently, because the Anthropic Economic Index gives it real data. The other two are where displacement is actually decided, and the model grows weaker the further it reaches into them. The trusted product wins before the best one does. The compliant product wins. The product embedded in a workflow wins. Capability is only one force in a larger institutional field, and a single timeline cannot show the gaps between the clocks, which is exactly where the strategic risk lives. Paper 02 made this point in a different vocabulary: technology becomes available, then individuals use it, then institutions redesign around it, and the distance between those stages is the story. TTD collapses that distance back into one figure.

The showcase example argues against the model, not for it.

Disney moves from 3.4 years to 11.7, presented as the Value Chain Audit working as designed. Read the other way, the same company, the same model, the same analyst produced two answers that differ by more than a factor of three, and the only thing that changed was a judgment about how to segment and weight revenue. That is not a measurement converging on a truth. It is an analyst’s prior, laundered through arithmetic until it acquires a decimal point. And the variable doing the work, revenue-weighted physicality, is itself a choice the model presents as a finding. The parks may be physically unsubstitutable while the narrative and emotional machinery that supports their pricing power becomes synthetic, personalized, and generated at home. The audit was right to reject “Disney is a media company.” It does not follow that physical revenue share is the dominant protective variable. A swing that large inside a single company should lower confidence in the output, not raise it.

A number designed to be wrong cannot also be a measurement.

The paper states plainly that the model is built around a self-fulfilling dynamic, that its intended effect is to motivate the action that renders its own prediction inaccurate. This is candid, and it is also fatal to the claim that the output is an estimate. A figure engineered to falsify itself when acted upon, and to be vindicated when it is not, confirms itself under every outcome. That is the property of a motivational device, not a forecast. The discipline the paper celebrates, forcing every strategic question into the open, is real at the moment the model is built. It quietly reverses at the moment the number is consumed, when “2.2 years” travels into a strategy deck with its assumptions stripped off and is repeated as a finding by people who never saw the judgment calls underneath it.

The borrowed mathematics carries credibility the inputs have not earned.

Options pricing earns its volatility term from decades of liquid, observable price data drawn from a distribution that is roughly stationary and symmetric. The paper concedes that AI capability volatility is none of these things. Importing the apparatus of Black-Scholes, whose validity rests on properties the new domain lacks, transfers the appearance of rigor rather than the rigor itself. Sigma means something there because it is estimated from a real return series. Here it is assigned. The same tension runs through the horizon factor, humanoid robotics near a threshold and agent-to-agent commerce arriving sooner than acknowledged, which is precisely the forward projection Paper 02 warned against when it argued that observed usage deserves more weight than theoretical capability. Multiplying a disciplined observed baseline by a speculative horizon term does not average the two. It lets the speculation set the result.

None of this means the displacement gap is unreal or even. It is both, and the four layers are a genuinely useful way to organize the conversation. The objection is narrower and harder. The move from organizing the conversation to closing it with a number is where rigor is lost rather than gained. The most expensive mistake here is not paralysis in the face of uncertainty. It is false confidence in the face of a decimal point, which ends the argument the model was built to start. What a board most needs is not the moment the clock runs out, but a reading of the several clocks that govern it: which one is closest, which assumption would have to break for the business to be in trouble, and how far the capability, adoption, and acceptance timelines have drifted apart. The future Paper 04 describes may not be less measurable than it claims. It may simply be measurable along more than one axis, and the distance between those axes is the part worth watching.

REFERENCES

Series and model

Peters, J. (2026). The Canary Papers 01: A Century in a Decade. Lightlabs.ai.

Peters, J. (2026). The Canary Papers 02: The Rate of AI Diffusion. Lightlabs.ai.

Peters, J. (2026). The Canary Papers 03: The Hidden Dependency. Lightlabs.ai.

The Canary Papers. Time to Displacement Methodology Companion. Internal methodology document.

Disruption frameworks and foundations

Schumpeter, J. A. (1942). Capitalism, Socialism and Democracy. Harper & Brothers.

Black, F., & Scholes, M. (1973). “The Pricing of Options and Corporate Liabilities.” Journal of Political Economy, 81(3), 637–654. https://www.journals.uchicago.edu/doi/10.1086/260062

Global Center for Digital Business Transformation (IMD and Cisco) (2015). Digital Vortex: How Digital Disruption Is Redefining Industries. https://www.cisco.com/c/dam/en/us/solutions/collateral/industry-solutions/digital-vortex-report.pdf

Boston Consulting Group and Moloco (2026). “Battle for the Interface: Introducing the Consumer AI Disruption Index.” https://www.bcg.com/publications/2026/introducing-the-consumer-ai-disruption-index (report PDF: https://web-assets.bcg.com/1a/d7/af023733403c96dfdb8a0d791bee/2026-02-06-moloco-report.pdf)

Boston Consulting Group (January 21, 2026). “Two-Thirds of Top Marketing Leaders Expect a High Level of AI-Driven Disruption to Consumer Behavior.” https://www.bcg.com/press/21january2026-marketing-leaders-expect-ai-driven-disruption-consumer-behavior

Reforge (July 9, 2025). “Is Your Product at Risk of AI Disruption?” (Use Case, Growth Model, Defensibility, Business Model). https://www.reforge.com/blog/ai-disruption-risk-assessment (assessment tool: https://ai-risk-assessment.vercel.app/)

AI pace, SaaS, martech, and the executive reversal

Griffin, K., remarks at Stanford (May 2026) and earlier at the World Economic Forum, Davos (January 2026), as reported in Fortune, “Billionaire Ken Griffin used to dismiss AI as ‘garbage.’ Here’s why he changed his mind, and why he’s ‘depressed,’” May 18, 2026. https://fortune.com/2026/05/18/billionaire-ken-griffin-ai-garbage-depressed-dramatic-impact-society/

Nadella, S., interview on the BG2 podcast with Brad Gerstner and Bill Gurley (December 2024), on the migration of business-application logic to an AI layer. [BG2 episode link to be inserted.]

Brinker, S., & Riemersma, F. (2025). 2025 Marketing Technology Landscape and State of Martech 2025 (15,384 solutions). https://content.martechday.com/state-of-martech-2025.pdf

Forbes (April 24, 2026). “SaaSpocalypse Is Dead: The Future of SaaS Is SaaS.”

Forrester (February 11, 2026). “SaaS as We Know It Is Dead: How to Survive the SaaS-pocalypse.”

Anthropic Economic Index and product cadence

Anthropic. “Anthropic Economic Index: Understanding AI’s Effects on the Economy.” Last updated March 24, 2026.

Anthropic, Massenkoff, M., & McCrory, P. (March 2026). “Labor Market Impacts of AI: A New Measure and Early Evidence.” https://www.anthropic.com/research/labor-market-impacts

Anthropic (January 13, 2026). “Introducing Anthropic Labs.”

Anthropic (April 17, 2026). “Introducing Claude Design,” and the associated decline in Figma (FIG) shares, as reported in Gizmodo, “Anthropic Launches Claude Design, Figma Stock Immediately Nosedives,” April 20, 2026. https://gizmodo.com/anthropic-launches-claude-design-figma-stock-immediately-nosedives-2000748071

Anthropic (April 28, 2026). “Claude for Creative Work.”

Anthropic (May 5, 2026). “Agents for Financial Services.”

Anthropic (May 13, 2026). “Introducing Claude for Small Business.”

Coursera, Udemy, and education services

Coursera, Inc. (May 11, 2026). “Coursera Completes Combination with Udemy to Build the World’s Most Comprehensive Skills Platform” (approximately $2.5 billion all-stock combination announced December 17, 2025; approximately 290 million learners, 18,000 enterprise customers, 95,000 content creators). https://investor.coursera.com/news/news-details/2026/Coursera-Completes-Combination-with-Udemy-to-Build-the-Worlds-Most-Comprehensive-Skills-Platform/default.aspx

Hart, G., comments to Axios on AI outpacing reskilling and the value of rigorous credentials, in “Coursera and Udemy complete merger to chase AI skills,” Axios, May 11, 2026. https://www.axios.com/2026/05/11/coursera-udemy-ai-skills

Reuters (December 17, 2025). “Coursera to Buy Udemy, Creating $2.5 Billion Firm to Target AI Training.”

Coursera Blog (September 9, 2025). “New AI-Powered Innovations on Coursera” (AI personas, course builder with approximately 87 percent reduction in course-creation time).

Coursera Blog (December 5, 2023). “Coursera Expands AI-Powered Translations” (translations across approximately 4,500 courses).

Coursera Investor Relations (November 18, 2025). “Coursera Partners with Anthropic to Drive Responsible AI Innovation and Workforce Transformation at Scale.”

OpenAI (October 6, 2025). “Introducing Apps in ChatGPT and the New Apps SDK” (Coursera as launch partner).

Disney and diversified revenue exposure

The Walt Disney Company. Form 10-K for the fiscal year ended September 27, 2025 (segment revenue: parks and experiences; media networks and streaming; studio entertainment; consumer products and direct-to-consumer). Filed November 2025.

The Walt Disney Company (November 13, 2025). “The Walt Disney Company Reports Fourth Quarter and Full Year Earnings for Fiscal 2025.”

The Walt Disney Company (December 11, 2025). “The Walt Disney Company and OpenAI Reach Landmark Agreement to Bring Beloved Characters from Across Disney’s Brands to Sora.”

Humanoid robotics and embodied AI

Figure AI (November 19, 2025). “F.02 Contributed to the Production of 30,000 Cars at BMW.”

Reuters (May 13, 2026). “Humanoid to Deploy Up to 2,000 Robots at Schaeffler Plants.”

Reuters (June 1, 2026). “Nvidia to Work with U.S., European Humanoid Robot Makers in Addition to China’s Unitree.”

Unitree Robotics (2026). “Unitree G1 Humanoid Robot.”

Agentic commerce and AI-mediated purchasing

OpenAI (September 29, 2025). “Buy It in ChatGPT: Instant Checkout and the Agentic Commerce Protocol.”

Stripe (September 29, 2025). “Stripe Powers Instant Checkout in ChatGPT and Releases Agentic Commerce Protocol Co-developed with OpenAI.”

Walmart (January 11, 2026). “Walmart and Google Turn AI Discovery Into Effortless Shopping Experiences.”

Morgan Stanley (December 8, 2025). “Agentic Commerce Impact Could Reach $385 Billion by 2030.”

The Canary Papers

The Canary Papers is a six-essay series drawn from executive conversations on AI adoption and strategic change. Named after the early detection systems once used in coal mines, the series focuses on signals rather than headlines, where capabilities are compounding, where organizations are lagging, and where competitive gaps are quietly widening. Each paper examines a distinct pressure point, from displacement timelines to diffusion barriers and trust costs. The aim is not prediction, but disciplined clarity: to help leaders recognize structural shifts early enough to act with intention rather than react under pressure.